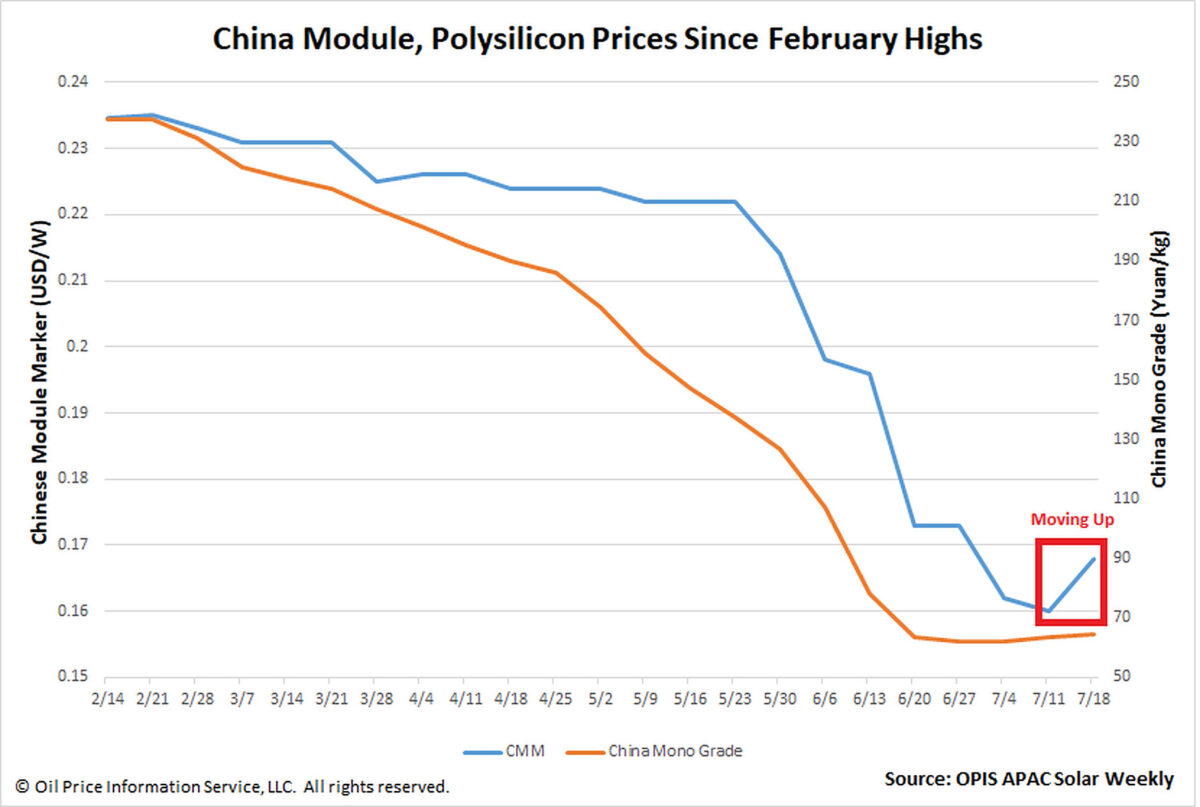

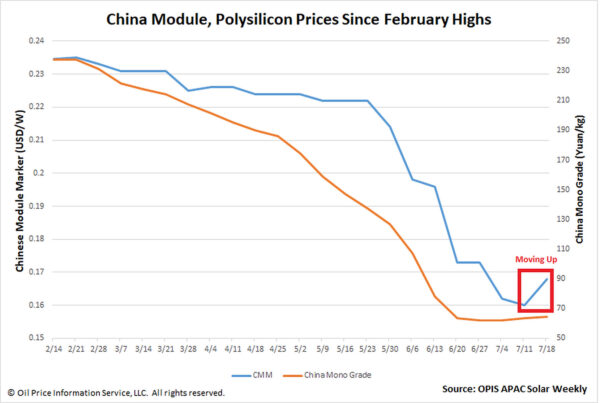

The Chinese Module Marker (CMM), the OPIS benchmark assessment for modules from China, rose to $0.168/W, in a week that saw the market contend with a weakening U.S. Dollar and growing prices across China’s solar value chain.

This 5% increase – CMM’s first move up in almost six months following recent record lows according to OPIS data – comes as most contacts noted prices of around $0.17/W and pointed to how the Dollar has depreciated in preceding days.

The upstream segments in China, from polysilicon down to cells, all saw gains this week, buoying module prices. China Mono Grade, OPIS’ assessment for polysilicon in the country, increased for a second week running to CNY64.42/kg, or almost $8/kg.

Module makers in China are raising production now, concurred multiple sources, although they offered different reasons for the move in the current low-price environment.

“Demand is rising now that prices are low,” with the third and fourth quarters a peak period for module sales, one source explained. Key export markets are exhibiting a normal growth rate, a solar industry veteran said. It is smaller, hardly-covered markets of below 1 GW each that, when combined, are driving demand, the veteran added.

For major tier-1 players, increasing production has “literally no correlation with demand,” according to a source at one such company. A Tier-1 manufacturer can squeeze smaller players out of the market and gain market share if it keeps on lowering its prices, according to an experienced market observer.

Moving forward, module prices are unlikely to keep rising as too many manufacturers mean intense competition in this sector, many contacts agreed. “In order to snatch orders, companies will choose to relinquish profits,” explained one source. Echoing the sentiment, another source said there isn’t much profit left to be taken, but it would be good if prices can stabilize at least.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.