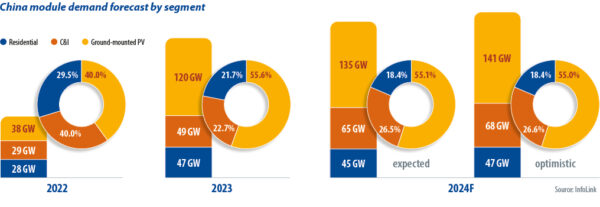

The Chinese solar market has witnessed rapid demand growth over the past two years. High PV module prices in 2022 hindered utility scale project deployment so small-scale, “distributed-generation” (DG) projects made up around 60% of the market. After supply chain issues eased, module prices started falling in 2023, driving utility scale projects that supplied 55% of the market in the fourth quarter while DG solar matured.

In 2024, China’s module demand will reach 245 GW to 255 GW, up 7% to 11% on 2023. Growth has slowed but the market is still huge. According to the National Energy Administration, China added 36.7 GW of solar in January 2024, and February 2024, up from 20 GW in January 2023 and February 2023. Ground-mounted projects drove a recovery in the market after the 2024 lunar new year holiday.

Some provinces capped grid connections for DG projects in the second half of 2023 and InfoLink believes the home solar market will slow in 2024. A national 5% cap on solar and wind power curtailment has been eased but rising curtailment will inject uncertainty into new project returns and grid capacity still lags behind solar demand.

The government’s Regulatory Measures for Grid Enterprises’ Full Purchase of Renewable Energy Electricity legislation categorizes grid-connected renewables projects into those with a guaranteed purchase volume of clean power and those subject to market trading for their electricity, affecting project returns. Long-term demand is being estimated conservatively and some DG end-users have canceled their plans.

Businesses seeking cost reductions could drive China’s commercial and industrial solar segment in 2024. Ground-mounted PV will depend on grid connections, even as provincial rules for agrivoltaics, fishery PV, and floating solar are being prepared.

While InfoLink anticipated no new polysilicon production capacity in the first quarter of 2024, producers such as Yongxiang, Daqo, and GCL are set to commission new lines in late June 2024 and second-quarter output could hit 250 GW to 255 GW, including an extra 79 GW to 80 GW in April 2024 and 84 GW to 85 GW in May 2024. Even with some manufacturers set to postpone poly lines, sales pressure and inventory pileup are likely.

Monthly wafer production of 65 GW to 68 GW in the second quarter will drive quarterly output of 200 GW to 205 GW. Some producers were planning to reduce output in April 2024 but vertically integrated manufacturers continue to scale production to maintain line operation and feed their cell and module businesses.

Cell production was expected to reach 200 GW to 210 GW during the second quarter, with monthly output of negatively-doped, “n-type” products set to hit 69 GW to 71 GW in April and May 2024. Deliveries became difficult from late March 2024 as module makers tried to control cost declines. Some module companies may have cut cell purchases via dual distribution in April 2024. Both features could resurface in the second quarter of 2024.

With more than 60 GW of monthly module production capacity in China, tier-1 manufacturers unable to reduce prices can reduce shipments. Tier-2 suppliers have modest plans for 170 GW to 175 GW of projects per quarter and could reduce production.

Regarding inventories, polysilicon reached a historic high of more than 20 days of stock on hand at the end of March 2024 and the figure will continue to rise. Wafer inventories were around half a month on hand and may have begun to slowly reduce from late April 2024, thanks to production cuts. Cell and module inventories were a healthy seven days and one to one-and-a-half months on hand, respectively, including stock in transit.

Competitive price

Overall, competition in the module sector is escalating in 2024, set against a backdrop of high inventory levels across the supply chain, surplus production capacity, and modest demand growth. Continuously falling module prices means InfoLink expects premiums for tunnel oxide passivated contact products to narrow and even to lead to the same price for n-type and older, positively-doped “p-type” modules on some projects.

Once the application of laser enhanced contact optimization becomes mature and replaces encapsulants in the second half of 2024, costs may go down marginally, enabling tier-1 prices to hover at CNY 0.85 ($0.12)/W to CNY 0.90/W in China. Meanwhile, severe competition in the low-price range may lead to a level lower than CNY 0.80/W in the market.

Module prices largely hinge on manufacturer strategies in 2024. Given the evidence supplied early in the second quarter, module makers appear to have become conservative in the face of low prices and weak profitability. Module producers may attempt to negotiate higher prices but end users, especially large customers, have a low tolerance for price hikes. For buyers, the industry hopes to establish a rule for adjusting the model of winning auctions with lower bids, given that prices have reached cost level, and some tier-2 module makers are competing with prices lower than cost, posing risks to order fulfillment.

About the author: Amy Fang is an InfoLink senior analyst who focuses on the solar cell and module segment of the PV supply chain, working across price trend forecasting and production data.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.