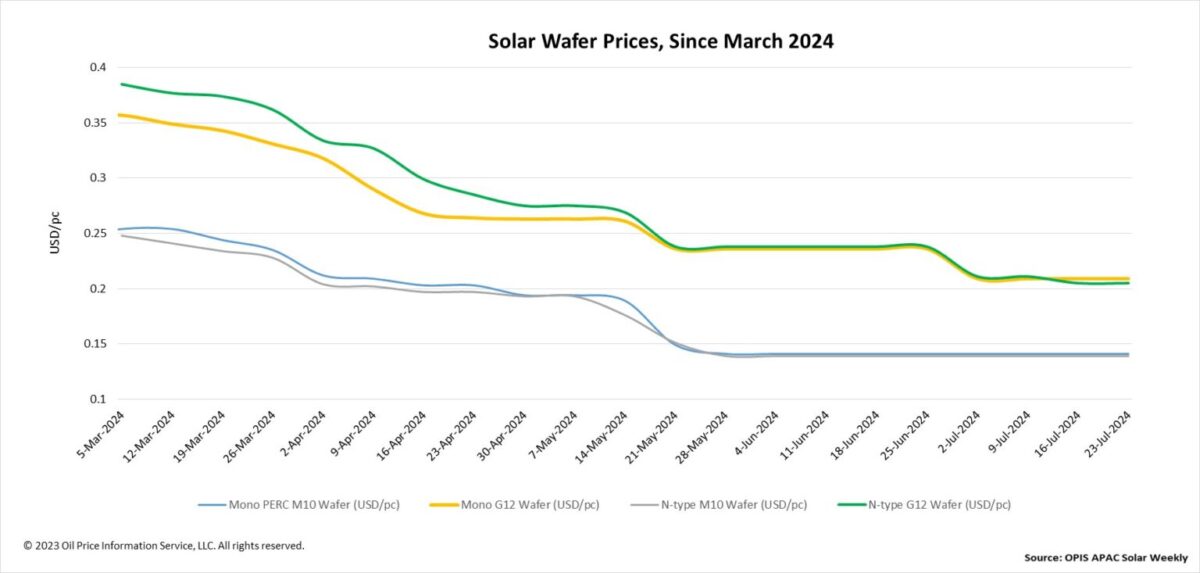

FOB China prices for wafers have remained stable across the board this week. Mono PERC M10 and n-type M10 wafer prices held steady at $0.141/pc and $0.139/pc, respectively. Likewise, Mono PERC G12 and nN-type G12 wafer prices remained unchanged at $0.209/pc and 0.205/pc, respectively, compared to the previous week.

Although there have been reports that n-type M10 wafer prices might increase due to the switch in China’s domestic wafer production lines from full square wafers sized 182 mm x 182mm to rectangular wafers sized 182 mm x 183.75mm and 182 mm x 210mm, actual transaction prices have remained unchanged except for a few companies’ increased offers.

“Given the sluggish downstream demand and the losses suffered by downstream companies, it is impossible to expect them to accept rises in upstream material costs,” a market source stated.

In contrast, the prices of n-type 210mm wafer set, including the full square 210 mm x 210mm wafers and rectangular 182 mm x 210mm wafers, have softened twice in the past month, according to the OPIS data. Industry insiders attribute this to a shift in production capacity from the 182mm set to the 210mm set, leading to increased inventory of the latter.

“As the market share of a size grows, its inventory rises and prices decrease, which the 210mm wafer set is currently experiencing,” a market observer commented.

According to the OPIS market survey, the majority of wafer operating rates in China’s domestic market are at 50% or lower, with the exception of a Tier-1 wafer producer and one big specialized wafer producer who maintains operating rates of more than 90%.

“Some integrated manufacturers who have halted in-house wafer production due to low market prices, are now sourcing most of their wafers from these two producers,” said a market participant.

A leading Chinese wafer manufacturer announced last week that it will establish a 20 GW ingot and wafering capacity in Saudi Arabia. According to an insider, it is expected the construction to begin this year, with completion and operation slated for 2026.

High gross margins from U.S. module prices are currently the only significant source of potential profitability for supply chain manufacturers, according to a market veteran, noting that this wafer project is expected to target the U.S. market in the future, potentially sourcing polysilicon from the three existing global polysilicon suppliers, the Oman and the UAE polysilicon plants yet to produce, and traceability-compliant Chinese regions.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.