India’s solar manufacturing capacity is poised for a healthy growth over the next two-three years, with 50 GW of PV cell and 80 GW of module manufacturing capacities, respectively, in the pipeline. This will necessitate a capex of INR 32,000 crore and INR 12,000 crore, respectively, says a new report by CareEdge Ratings.

Coupled with the cumulative capex of INR 55,000 crore envisioned for over 40 GW of wafer and 25 GW of polysilicon capacities awarded under the production-linked incentive (PLI) scheme, the solar equipment sector will witness a capex of close to INR 1 lakh crore, with an estimated debt funding of nearly INR 70,000 crore over the next 3-5 years.

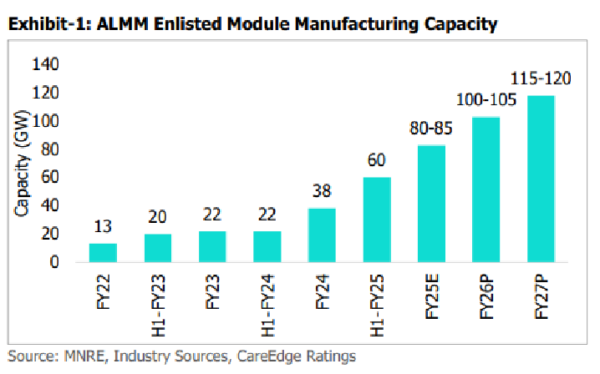

The nation’s module and cell capacity stood at 70 GW (with high-efficiency module capacity forming 50 GW) and 8 GW, respectively, as of March 2024. The capacity listed under the Approved List of Models and Manufacturers for modules (ALMM-I) reached 60 GW as of Sept. 2024, but a large chunk is in the ramp-up phase.

With the addition of pipeline capacity, domestic cell capacity is expected to reach 60 GW by FY27. “The resultant capacity growth will make India a surplus market, given the annual module requirement of 40-50 GW, necessitating that the domestic players tap the export markets,” says the report.

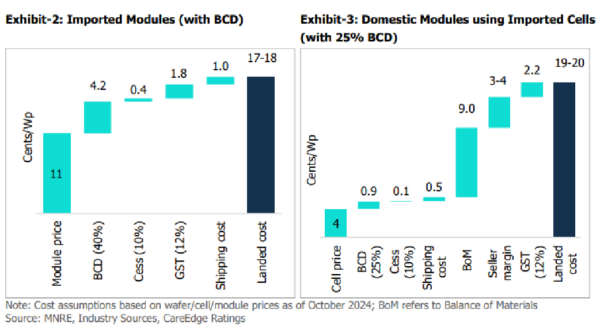

The report says while the imposition of tariff barrier like basic customs duty (25% and 40% on Chinese cells and modules, respectively) has increased the cost-competitiveness of domestic cells and modules, the impact is partly offset by a steep fall in global module prices over the last two years.

“While BCD increases the landed cost by 4-5 cents/Wp for imported modules and 1-2 cents/Wp for imported cells, DCR modules (modules complying with domestic content requirement) are pricier than both imported as well as non-DCR modules on a landed basis,” states the report.

Imported modules remain cheaper than domestic modules by 8-10% despite the applicable duties. However, the report adds, non-tariff barriers like Approved List of Models and Manufacturers for solar modules and government-sponsored schemes like CPSU scheme, PM KUSUM and PM Surya Ghar Muft Bijli are likely to push demand for domestic modules.

Under ALMM-I mandate, domestic modules are compulsory for all solar projects in the country, except for utility-scale projects awarded before March 10, 2021, and open access and net metering projects that had secured key approvals before Oct. 1, 2022.

Moreover, the government has proposed to implement ALMM-II, which mandates the use of domestic cells in locally assembled modules, from June 2026, effectively making DCR modules mandatory for all solar capacities.

The report states that the introduction of ALMM-II for domestic cells may result in increasing the delivered cost of domestic modules by 6-7 cents/Wp, leading to a rise in solar tariffs by 40-50 paise per unit for the short term till local cell supply scales up.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.