The global solar manufacturing sector is rapidly expanding, driven by technological advancements, cost reductions, and increased government support. Rising greenhouse gas emissions have intensified the need for clean energy solutions, positioning solar power as a key focus in the fight against climate change. As countries work to meet their climate goals under the Paris Agreement and prioritize clean energy, the need for domestic manufacturing has grown to reduce import dependence and enhance energy security.

Solar landscape in India

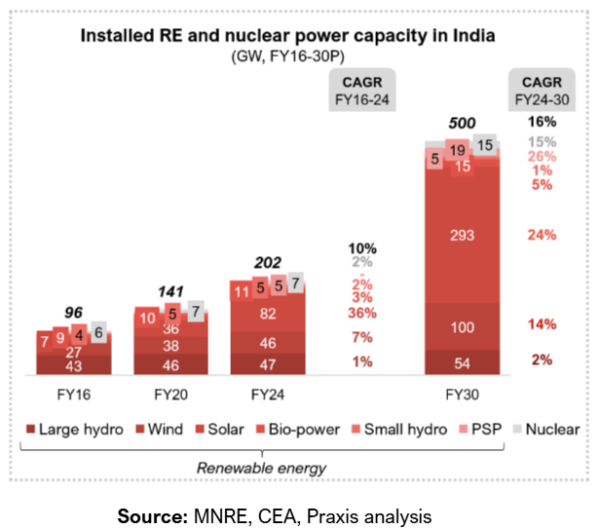

India’s ambition to achieve 500 GW of renewable energy by 2030 hinges significantly on solar power, which is projected to account for over 60% of the total capacity. To meet this target, India must scale its solar installations to 50-60 GW annually.

By FY24, India had installed over 80 GW of solar capacity. However, the country faces major challenges in meeting this demand domestically, as its solar manufacturing sector remains heavily reliant on imports, particularly from China.

In 2023 alone, India added 20.8 GW of solar module capacity and 3.2 GW of solar cell capacity. Projections suggest that within the next 5 years, India’s solar module manufacturing capacity will exceed 150 GW, and solar cell capacity will surpass 75 GW – critical steps toward reducing import dependence and achieving renewable energy goals.

However, India’s solar manufacturing sector primarily assembles solar modules from imported components, such as polysilicon and wafers, resulting in only 30-40% local value addition. Furthermore, the country does not produce solar cells using indigenous raw materials, like silica sand, which deepens its import dependency. As a result, India’s domestic manufacturing sector operates at just 40-45% capacity utilization, with an operational output of 7 GW that meets only about 35% of domestic demand.

Players like Adani, Waaree, and others have now shifted their focus toward manufacturing the entire solar value chain domestically (from silica to modules), potentially increasing India’s local value addition share by 2030.

Global landscape for solar manufacturing

Governments and companies across the globe are aiming to integrate the entire value chain in-house to lower costs, improve operational efficiency, and generate more job opportunities. Although, this strategy from various countries faces significant barriers from China’s stronghold, ever-evolving technologies, and mature export market in this space.

China’s stronghold over solar manufacturing value chain

China’s competitive advantage stems from its large-scale production, low electricity costs, and fully integrated manufacturing process, which allows Chinese companies to offer solar equipment at lower prices than Indian manufacturers.

Additionally, China’s substantial investments in R&D and strong government incentives position it as the dominant player in the global solar market, controlling more than 80% of global solar production. China can produce solar modules at costs 30-65% lower than the US and Europe, which gives the country a competitive advantage in the global market.

Global solar PV manufacturing capacity has increasingly moved from Europe, Japan, and the United States to China over the last decade. China has invested over US$ 50 billion in new PV supply capacity, ten times more than Europe.

Ever-evolving photovoltaic technology

While Passivated Emitter and Rear Contact (PERC) cells remain dominant, innovations like n-type based TOPCon and Silicon Heterojunction (SHJ) cells are gaining momentum due to their higher efficiency and better performance at lower costs. Additionally, breakthroughs such as perovskite-silicon tandem solar cells, which exceed 30% efficiency, are emerging (module life is currently limiting its implementation).

These next-generation technologies promise significant improvements in efficiency, material usage, and power output, positioning them as key drivers for global growth in solar energy.

Currently, monocrystalline modules account for 67.5% of India’s total PV panel production. Polycrystalline modules follow at 15.1%, while Tunnel Oxide Passivated Contact (TOPCon) modules and thin-film technologies make up smaller shares of 12.3% and 5.1%, respectively.

China, on the other hand, has increasingly transitioned to n-type based technologies (TOPCon and SHJ) reaping cost efficiencies at scale.

Mature export market and India’s dependency

China’s solar module exports have risen 34% YoY, growing from 85 GW in the first half of 2022 to 114 GW in the same period this year, almost matching the total exports of 2021. This volume could power Sweden and is equivalent to the entire solar capacity of the US (113 GW).

In 2023, India imported 16.2 GW of solar modules, a 158% year-over-year increase, and 15.6 GW of solar cells, up from 5.8 GW in 2022. India’s solar module exports reached 4.8 GW in 2023, a 204% increase from 2022. However, these exports remain modest compared to the volume of imports, highlighting the ongoing limitations of India’s domestic manufacturing capabilities.

China is India’s largest supplier, providing US$ 3.89B worth of solar cells and modules, which accounts for 62.6% of total imports. It is followed by Vietnam (US$ 1.02B, 16.5%), Malaysia (US$ 549.8M, 8.9%), and Thailand (US$ 248.8M, 4%).

Strategies to transition towards domestic manufacturing

Friendly regulatory policies

Governments across the globe are implementing friendly monetary policies to develop local manufacturing infrastructure, although the scale of these initiatives has varied across geographies.

The Indian government has introduced the Approved List of Models and Manufacturers (ALMM) and the Production-Linked Incentive (PLI) schemes to incentivize local manufacturing, protect domestic manufacturers, and maintain quality standards. These measures are designed to reduce import dependency and improve the efficiency and sustainability of India’s solar manufacturing sector.

Inflation Reduction Act (IRA) in USA, outlays investment in manufacturing and assembling key renewable energy parts such as solar panels, wind turbines, etc. Investment and production in clean energy sources to get PTC and ITC benefits by employing domestic labor. Credit tax of up to 30% is provided to manufacturers. IRA aims to invest US$ 50 billion to increase domestic manufacturing in the country.

China provides various subsidies, tax rebates, and low-interest loans to solar PV manufacturers. These incentives have allowed local companies to invest in advanced manufacturing technologies, helping them stay competitive in the global market.

Trade restrictions to decrease China’s influence

Countries worldwide are increasingly implementing customs duties as a strategy to curb imports, protect local industries, and promote domestic growth. These sanctions are only expected to increase further as China continues to dominate the space.

The Indian government has imposed a 40 percent customs duty on Chinese solar modules and 25 percent on solar cells, driving up installation costs by 20–30 percent and slowing project growth. Notably, India has maintained similarly high duties on imported cars—100 percent for those priced above USD 40K, 60 percent for those below, and 125 percent on used cars—indicating that such high tariffs on solar imports are unlikely to be temporary and could even increase over time.” “

In the US a tariff of 50% has been proposed for polysilicon used in solar panels starting 2025. Most US solar panel imports now come from Southeast Asia. Washington has doubled tariffs on Chinese panels to 50%.

Conclusion

India must also focus on boosting upstream solar production, from raw materials like silica sand to the manufacturing of finished solar panels. By building domestic capabilities to produce polysilicon, wafers, and cells, India can reduce its reliance on imports and improve the cost efficiency of its solar manufacturing sector.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

Your article on the Top 15 Solar PV Panel Manufacturers in India is incredibly informative and well-researched. It’s great to see a detailed overview that highlights the strengths of each company.