Solar, wind, and energy storage manufacturers have all entered 2025 facing manufacturing oversupply and fierce competition on price. Lithium-ion battery cell producers are not insulated from the trend yet there are reasons to expect that market conditions for manufacturers will improve as consolidation occurs and demand continues to expand, Sam Wilkinson, a Director Clean Energy Technology, at S&P Global Commodity Insights told ESS News.

Last week S&P Global outlined its expectations for clean technology marketplaces, in its Top Clean Trends for 2025 report. It paints a picture of market and investment growth at the same time as manufacturers grapple with falling prices.

“There is an oversupply in the battery market right now. But I would argue that no high growth market in its early stages will ever have supply and demand perfectly balanced,” said Wilkinson. “But at some point in the next few years we will almost certainly see the reverse, once demand reacts to the low prices, which it already is starting to do.”

Benefits of scale

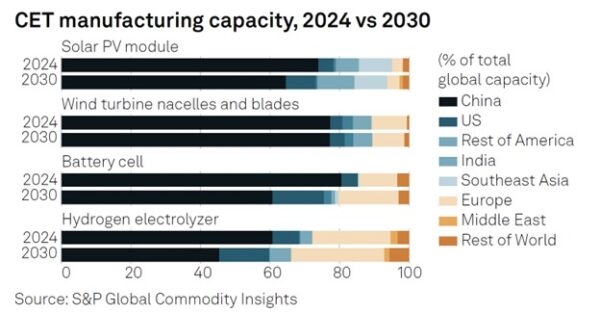

S&P Global reports that global lithium-ion battery annual production output surpassed 10 billion cells for the first time in 2024, the cause of both the oversupply and cost reductions as a result of scale.

“Based on some estimates and back of the envelope calculations, you see that global lithium-ion battery cell production in 2024 was around 11 billion units. That’s the type of volume that enables you to drive down costs and what makes innovation so powerful. When you’re making things in that volume, just a tiny incremental increase in efficiency or output or throughput or performance or reliability is magnified. It enables you to go along that learning curve.”

Nickel manganese cobalt (NMC) still accounts for the majority of lithium-ion battery cell production, for supply to the EV market. However, the expansion of stationary storage applications, both distributed and at utility scale, is seeing lithium iron phosphate (LFP) play an increasingly prominent role in battery manufacturing. LFP is also seeing greater acceptance in the EV market. And vertical integration is seeing LFP makers rapidly innovate with increased energy densities and reduced cost.

“[Stationary] energy storage went from being something like 10% [of LFP production] a few years ago to 25% of global output in 2024. And that’s a trend that continues into 2025,” said Wilkinson. “What that means is that the lithium-ion battery manufacturing giants are now focusing on it. They’re innovating when it comes to producing energy storage products specifically.”

Wilkinson notes that while containerised utility-scale battery systems, in a standard 20-foot format, had capacities of 2 to 3 MWh of capacity earlier this decade, leading producers are now announcing products with up to 6 to 8 MWh.

Article continues on pv magazine’s ESS News…

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.