A new report by SBICAPS projects India’s annual solar capacity addition to double to 30 GW in FY25 against 15 GW in FY24.

The report states the deployment pace will further improve in FY26 and FY27, leading to significant spike in module demand. It projects PV deployment for FY26 at 42 GW and for FY27 at 46 GW, with residential rooftop solar driving expansion.

Annual module demand is forecast to increase from 50-55 GW in FY 2025 to 105 GW in FY 27. [The calculation assumes DC/AC overloading of 1.2-1.4, effective utilization to nameplate capacity ratio of 55-65%.]

The report says PV installation projections are likely to be met with moderate PPA-PSA gap reduction, PM Surya Ghar Muft Bijlee Yojana (PM-SGMBY) completion by FY28, and enhanced RPO [renewable energy purchase obligation] compliance. Timely scheme (especially PM-KUSUM) and project execution could further augment demand. On the other hand, land constraints, ALCM [Approved List of Cell Manufacturers] implementation, and restrictive state net metering policies pose as deterrents.

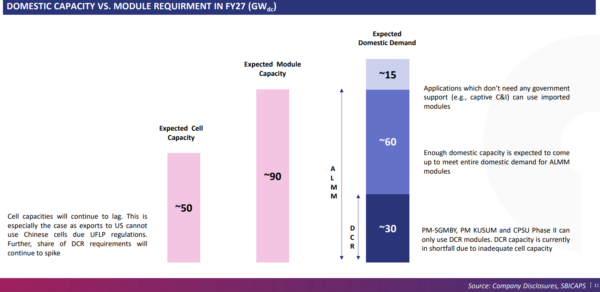

Cell capacities will continue to lag

The report states that the module ecosystem will reach maturity as it hits an effective capacity of 90-100 GW by FY 27, which is sufficient to meet the entire domestic demand for ALMM modules. The remainder demand, consisting largely of C&I captive segment, may be met with cheaper imports as these applications don’t need any government support and therefore can use imported modules.

“Major module makers have announced significant capacity increases, which will take their nameplate capacity from 90-100 GW now to 150-160 GW by FY27. The latter translates to an effective capacity of 90-100 GW by FY 27,” states the report.

Cell capacity will reach 50 GW by FY 2027, lagging behind the module capacity of 100 GW.

The report says the integration drive needs to kick into next gear to meet ALCM and DCR goals. [DCR solar panels are panels made in India with domestically manufactured cells, meeting the domestic content requirement as stipulated for PV installations under PM Surya Ghar Muft Bijlee Yojana, PM KUSUM and CPSU Phase II Scheme.]

“Despite integration factor (cell/module capacity ratio) likely improving from 32% to 65%, more than half of India’s cell requirements will continue to be imported in FY27, even if all capacities promised come on board,” states the report.

DCR module prices will maintain a premium due to PM-SGMBY-driven demand exceeding cell capacity additions and escalating regulatory stringency on DCR. As cell production expands, wafer and ingot manufacturing emerge as the next strategic imperative, with the government expected to allocate $ 1 billion in incentives to foster domestic ecosystem development.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

1 comment

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.