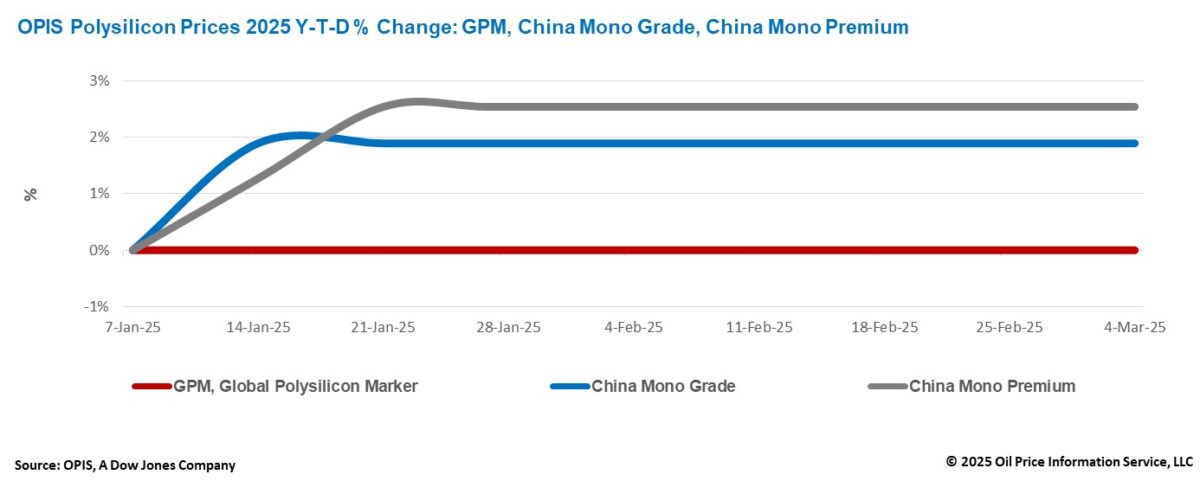

The Global Polysilicon Marker (GPM), the OPIS benchmark for polysilicon produced outside of China, remained steady this week at $20.360/kg, or $0.046/W, reflecting unchanged market fundamentals.

Trade sources reported current transaction prices between $18/kg ($0.041/W) and $21/kg ($0.047/W), with one supplier’s price holding below $20/kg ($0.045/W).

While the global polysilicon market maintains its stability, market participants are closely monitoring the potential impact of several unresolved U.S. trade policies, which could drive up GPM polysilicon demand. These include the potential Section 232 tariff investigation on solar products, possible expansions to the non-traceability compliant entity list, final rulings on anti-dumping and countervailing duties (AD/CVD) for solar products imported from Vietnam, Cambodia, Malaysia, and Thailand, and speculation about similar AD/CVD investigations targeting Indonesia, Laos, and India.

According to market sources, the potential Section 232 tariff investigation on solar-related products beyond steel and aluminum, namely polysilicon, is expected to last approximately nine months once initiated. However, its impact may be felt much earlier, well before the formal implementation of the policy.

Certain major buyers, despite incurring losses, are reportedly continuing to meet their long-term agreements with global polysilicon suppliers through monthly orders. Sources suggest these buyers are mentally prepared for potential policy shifts and are strategically positioning themselves for future market changes.

The U.S. announced a new 10% tariff last week, effective March 4, which will be added to existing duties on Chinese imports. This move will raise the total tariffs on Chinese polysilicon, wafers, cells, and panels to approximately 84%, considering additional tariffs under Section 201 and Section 301.

While this development is not expected to significantly alter current trade patterns in the global polysilicon market, the broader trend of increasing restrictions on products containing Chinese components could ultimately support demand for GPM polysilicon.

The China Mono Grade, OPIS’ assessment for mono-grade polysilicon prices within the country, remained stable this week at CNY 33.625/kg, equivalent to CNY 0.076/W. Similarly, the China Mono Premium, OPIS’ price assessment for mono-grade polysilicon used in N-type ingot production, held steady at CNY 40.375/kg, or CNY 0.091/W.

Industry feedback indicates that the highest signed sales order for N-type polysilicon currently stands at CNY 43/kg (CNY 0.097/W), while the bundled price for N-type and P-type polysilicon is still around CNY 38/kg (CNY 0.086/W).

The stability in polysilicon prices is attributed to unchanged supply and demand dynamics. Sources noted that maintaining a low operating rate is not only a regulatory requirement but also a strategic move based on production cost considerations. A top-four manufacturer estimated that operating its full annual production capacity of 300,000 metric tons (mt) would result in a monthly loss of nearly CNY 600 million, highlighting the economic rationale for limiting production.

Consequently, polysilicon manufacturers are expected to maintain low operating rates, generally around 30% to 40%, until prices rise further. Increasing production under current pricing and demand conditions would only increase inventory and consume cash.

At the end of February, polysilicon inventory reportedly stood at approximately 300,000 mt, with more than half -around 180,000 mt – held by wafer factories. Additionally, trade sources project monthly polysilicon production to remain at about 100,000 mt in the coming months, corresponding to approximately 50 GW of wafers production per month. This indicates that clearing the existing polysilicon inventory could take considerable time.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.