India’s cumulative installed open-access (off-site) solar capacity reached 20.2 GW at the end of 2024. The market is set for significant expansion driven by corporates’ sustainability goals and favorable economic and policy factors.

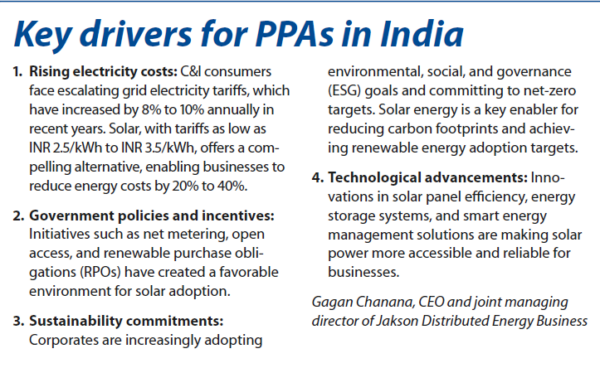

“This substantial growth is driven by escalating grid tariffs, which, in some regions, have increased by up to 15% annually. Combined with the decreasing cost of solar modules, which have fallen by nearly 30% in the last two years, the economic case is compelling,” said Gagan Chanana, CEO and joint managing director of Jakson Distributed Energy Business.

“With India’s ambitious renewable energy targets, we anticipate the C&I sector to contribute significantly, potentially accounting for more than 30% of new solar installations over the next five years.”

Commercial models

The two preferred solar procurement models are ownership and power purchase agreement (PPA). Sharad Gupta, vice president design, engineering and execution at Oorjan Cleantech, said that under the ownership model, the business invests in the solar infrastructure and owns the asset, working with an engineering, procurement, and construction (EPC) company for installation. This arrangement offers the most long-term savings and return on investment (ROI) over the lifespan of the system, which is

typically 25 years. Ownership is therefore preferred by companies with available capital.

Under the PPA model, a third-party developer installs, operates, and maintains the solar plant, delivering power to the business customer at a fixed rate –usually lower than the grid tariff – over

a period typically lasting 10 to 25 years. While the PPA rates are usually fixed, sometimes the agreement has a provision for a slight annual increase in price to account for inflation. Thus, the C&I entity benefits from reduced electricity costs without making a large initial investment in the PV system.

Open access

The open access (off-site solar) mode is gaining momentum among large consumers and those with space constraints. It allows them to procure solar power from off-site solar plants through long-term PPAs with the developers setting up the plants.

“Rooftop solar installations pose structural constraints on the property offered for the project,” said Gupta. “Open-access solar projects are a valid option for companies with minimal roof capacity.”

The Green Energy Open Access (GEOA) Rules, implemented by the Ministry of Power in June 2022, specify a minimum contracted demand of 100 kW for open access. Subsequent amendments enabled demand aggregation through multiple connections, driving significant interest from smaller consumers.

According to a recent report by Mercom, India’s cumulative installed open access solar capacity reached 20.2 GW by the end of 2024. The pipeline passed 25.7 GW (under development and pre-construction).

The states with the most project activity were Gujarat, Karnataka, Maharashtra, Rajasthan and Tamil Nadu.

Open-access solar is not without challenges. Land acquisition, state deviations from central rules –especially with regard to open access eligibility threshold, approval timelines, and charges – and inadequate transmission infrastructure are the key factors constraining the open access solar segment in some regions.

At the same time, falling solar panel costs have made the capital expenditure model attractive to business.

“C&I installations, particularly those focused on on-site generation, are increasingly choosing advanced solar technologies like n-type TOPCon modules ranging from 560 W to 600 W, [and also] mono PERC half-cut bifacial PV modules, typically between 500 W and 550 W, based on specific site conditions,” said Akshay Mittal, director of Bluebird Solar. “These high-wattage modules are favored for their exceptional efficiency, which enables businesses to maximize energy production in limited rooftop spaces, a common challenge in commercial and industrial environments.”

Battery storage is also becoming increasingly important. Integration with battery energy storage systems is set to gain traction with rapid technology advancements and a fall in prices. “Advancements in energy storage systems are likely to make solar-plus-storage solutions viable for round-the-clock power, while solar-driven green hydrogen is emerging as a key decarbonization tool for energy-intensive industries,” said Chanana.

In the future, Chanana expects the C&I solar sector to play a major role in India’s 500 GW renewable energy target by 2030.

The growth in this segment will especially be driven by industries with high energy consumption, cost-saving potential, and sustainability commitments.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.