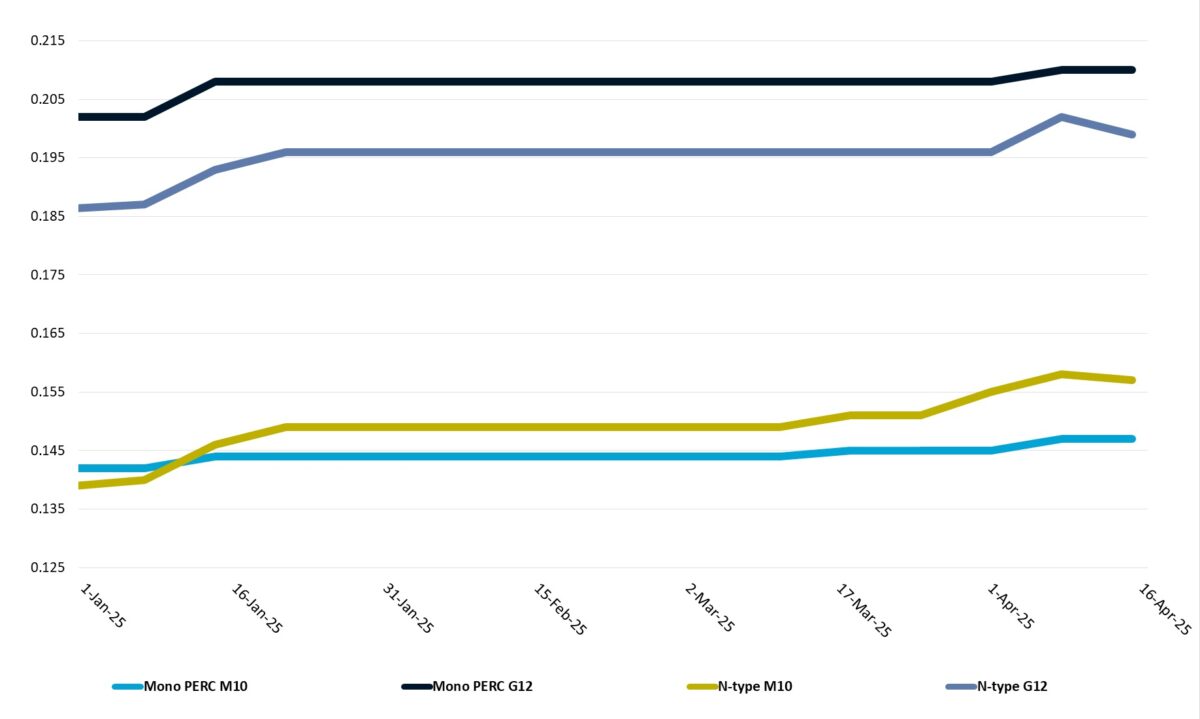

FOB China prices for Mono PERC wafers remained stable this week, with M10 and G12 wafers holding steady at $0.147/pc (per piece) and $0.210/pc, respectively. In contrast, FOB China prices for N-type wafers experienced a decline. N-type M10 wafers fell to $0.157/pc, while G12 wafers dropped to $0.199/pc, reflecting week-on-week decreases of 0.63% and 1.49%, respectively.

The recent surge in end-user installation demand in China – driven by two solar power policies scheduled to take effect in May and June – is reportedly drawing to a close. This easing in demand has led to a more relaxed supply environment in the wafer market and contributed to this week’s decline in prices.

Meanwhile, China’s wafer production output for April, initially projected at approximately 57 GW due to the anticipated disruption from the Myanmar earthquake, has been revised upward to around 61 GW based on updated production schedules from wafer manufacturers. Industry sources indicate that the sector’s surplus production capacity has effectively absorbed the impact of the disruption. These developments have further reinforced the prevailing pessimism regarding the outlook for China’s wafer market.

In the global market, U.S. President Donald Trump has announced a three-month suspension of all “reciprocal” tariffs, with the exception of those applied to China. As a result, countries such as Laos and Indonesia, key recipients of Southeast Asian wafers, will face only a 10% baseline tariff on cells and modules exported to the U.S. during this window.

While no official confirmation has been issued by manufacturers, industry insiders widely speculate that wafer production rates in Southeast Asia are likely to increase in the short term. The aim is to expedite shipments to regions outside the four countries targeted by the AD/CVD investigation, where wafers can be further processed into cells and modules and delivered to the U.S. before the three-month tariff reprieve ends.

In the long term, evolving international trade policies are expected to reshape the export landscape for Chinese and Southeast Asian silicon wafers. Beyond serving local market demand, the U.S. market will remain a critical export destination of solar cells, as domestic cell production in the U.S. continues to fall short of meeting the requirements of its module manufacturing sector. Consequently, the U.S. is likely to maintain its reliance on imported cells, primarily from countries subject to relatively lower comprehensive tariffs.

Regions such as South Korea, India, Egypt, Ethiopia, Turkey, Saudi Arabia, and Oman – where solar cell production is either already established or currently under development – are expected to emerge as key destinations for wafer exports. Market sources highlight that these regions offer favorable tariff environments and are likely to play an increasingly important role in global wafer trade flows.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.