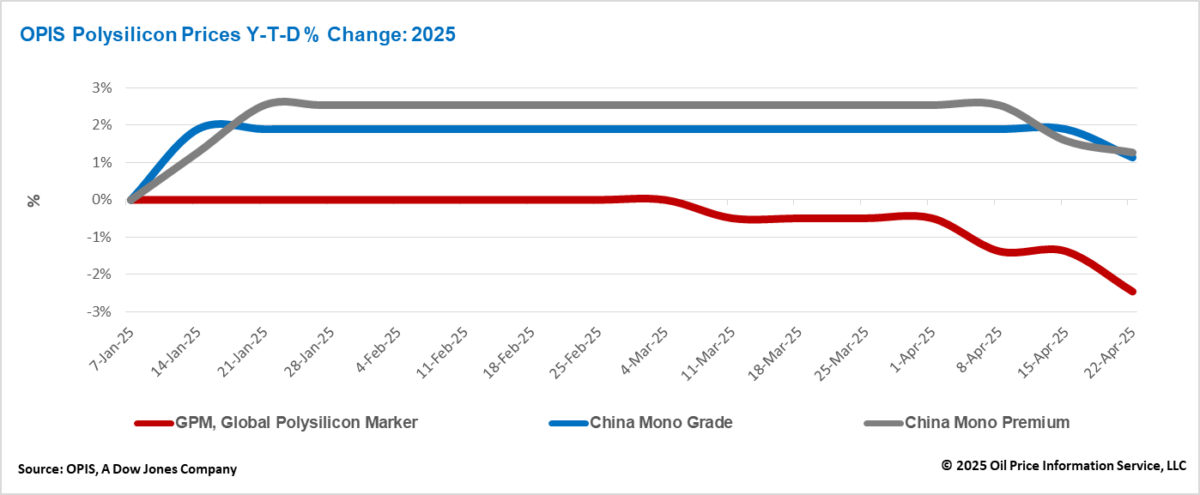

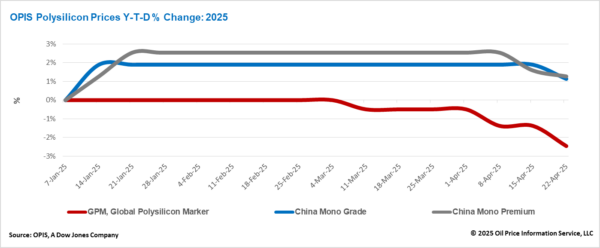

The Global Polysilicon Marker (GPM), the OPIS benchmark for polysilicon produced outside of China, was assessed at $19.860/kg or $0.042/W this week, reflecting a 1.10% decline based on reported buy-sell indications.

The prevailing pessimism in the global polysilicon market continues to intensify, with current conditions still favoring buyers to a certain extent, allowing them to retain a degree of leverage in negotiations.

Buyers—particularly those tied to long-term agreements—are reportedly showing a stronger inclination to push for price reductions, a trend largely attributed by industry insiders to the impact of rising tariffs on end products exported to the U.S.

Despite this pressure on long-term pricing, small volumes of spot transactions outside such agreements continue to emerge. According to trading sources, the lowest prices in these deals are still trending downward. Market participants believe these spot purchases reflect strategic planning by certain buyers. In light of increasing U.S. restrictions on products containing Chinese components, these buyers are proactively securing low-cost materials and diversifying their supply chains to mitigate potential risks posed by stricter trade measures.

Contrary to earlier market speculation, the three-month suspension of reciprocal tariffs by the U.S. has so far failed to significantly stimulate wafer production in Southeast Asia. Consequently, the anticipated short-term boost in global polysilicon demand has not materialized. According to a major integrated manufacturer, the current wafer production levels in Southeast Asia are sufficient to support the limited solar cell output currently eligible for export to the U.S.—an output that remains concentrated in only a handful of countries.

The China Mono Grade, OPIS’ assessment for mono-grade polysilicon prices within the country, fell by 0.74% this week to CNY 33.375 ($4.57)/kg, equivalent to CNY 0.070/W. Likewise, the China Mono Premium, OPIS’ price assessment for mono-grade polysilicon used in n-type ingot production, declined by 0.31% week-on-week to CNY 39.875/kg, or CNY 0.084/W. This price reduction is primarily attributed to the weakening downstream demand and the ongoing issue of oversupply.

The current transaction volume of polysilicon reportedly remains very low, and market participants anticipate that large-scale polysilicon transactions may not resume until late May. This is primarily due to the fact that, based on the current wafer operating rates, existing polysilicon inventories held by wafer manufacturers are sufficient to sustain production for more than a month.

Major polysilicon manufacturers reportedly plan to maintain their current low operating rates at around 40%. According to market sources, production is expected to increase in the Sichuan and Yunnan regions during the upcoming wet season, which brings significant electricity price discounts. However, to avoid a substantial rise in overall output, manufacturers will simultaneously carry out maintenance at facilities located in regions dependent on thermal power, thereby carefully managing total production levels.

Broader pessimism surrounding market demand in 2025 is now exerting downward pressure on China’s polysilicon futures market. According to data released by the Guangzhou Futures Exchange on April 21, futures prices for polysilicon deliveries from June 2025 through April 2026 have all dropped below CNY 40/kg. The highest settlement price, for June 2025 delivery, stood at CNY 37.89/kg, down 15.39% from its January 17 peak of CNY 44.78/kg. This price also represents a 4.98% discount compared to the latest spot price assessed by OPIS this week.

OPIS, a Dow Jones company, provides energy prices, news, data, and analysis on gasoline, diesel, jet fuel, LPG/NGL, coal, metals, and chemicals, as well as renewable fuels and environmental commodities. It acquired pricing data assets from Singapore Solar Exchange in 2022 and now publishes the OPIS APAC Solar Weekly Report.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

By submitting this form you agree to pv magazine using your data for the purposes of publishing your comment.

Your personal data will only be disclosed or otherwise transmitted to third parties for the purposes of spam filtering or if this is necessary for technical maintenance of the website. Any other transfer to third parties will not take place unless this is justified on the basis of applicable data protection regulations or if pv magazine is legally obliged to do so.

You may revoke this consent at any time with effect for the future, in which case your personal data will be deleted immediately. Otherwise, your data will be deleted if pv magazine has processed your request or the purpose of data storage is fulfilled.

Further information on data privacy can be found in our Data Protection Policy.