The importance of solar mini-grids in universalizing energy access

As solar energy becomes the most cost-effective form of energy generation in many countries, with clear climate, energy, and economic benefits, its acceptance and political support are growing. To enhance resilience and sustainability, strategies that incorporate a diverse energy mix, combining centralized and distributed renewable generation, are most effective, especially in underserved nations.

Government considering viability gap funding, ALMM mandate for battery storage projects

The Indian government is considering financial incentives such as viability gap funding and green finance to encourage the adoption of energy storage systems in the country. It may also issue an Approved List of Models and Manufacturers (ALMM) mandate for battery storage systems for power sector applications.

Ghaziabad to be developed as Uttar Pradesh’s next solar city after Ayodhya

The city will meet 10% of its electricity requirements from solar power in four years.

Australia backs 248 GW pipeline to counter reliability challenges

The Australian Energy Market Operator (AEMO) says that 248 GW of proposed generation projects, storage installations, transmission developments, and government energy programs have the potential to address many of the risks in its latest market forecast – if they are delivered to schedule.

USA, India launch renewable energy technology action platform

The renewable energy technology action platform will initially focus on green and clean hydrogen, wind energy, long-duration energy storage, and exploration of geothermal energy, ocean/tidal energy and other emerging technologies.

Annual renewables installations to surge 33% to 20 GW this fiscal

India is expected to add around 20 GW of new renewable energy capacity (16 GW solar and the balance wind) in FY 2024. This is 33% up from 15 GW installed in FY 2023.

HSBC announces $2 million funding to IIT Bombay, Shakti Sustainable Energy for green hydrogen innovation

HSBC India has partnered with the Indian Institute of Technology (IIT) Bombay to support innovation-led green hydrogen initiatives. It has also partnered with Shakti Sustainable Energy Foundation (SSEF) to support policy research, and technological and financial solutions for real-world application of green hydrogen in industrial clusters across four states of India.

The Hydrogen Stream: New way to make drug materials from hydrogen

UW–Madison has developed an environmentally friendly approach for producing essential drug ingredients by opting for hydrogen, while India has presented new green hydrogen standards.

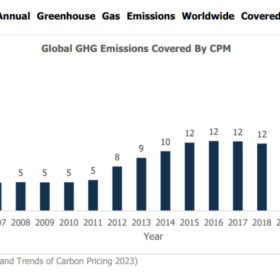

Unveiling India’s carbon credit revolution: From local initiatives to global impact

The Indian carbon credit system, operating under the Clean Development Mechanism (CDM) and the United Nations Framework Convention on Climate Change (UNFCCC), stands ahead in several aspects.

Deployment trumps solar manufacturing in EU priorities

A lack of clear policy support, raw material dependency, and higher production costs are inhibiting the localization of European solar manufacturing, despite strong demand.