Driving renewable energy adoption: Challenges and opportunities

India’s robust economic growth translates to rising demand for energy. This demand provides a substantial market for renewable energy investments, encouraging firms to venture into this sector. However, as the nation marches ahead in RE adoption, it needs to overcome challenges like high capital costs and inadequate grid infrastructure.

Top 5 solar inverter suppliers accounted for 71% of global shipments in 2022

Huawei, Sungrow, Ginlong, Solis, Growatt, and GoodWe emerged as the top solar inverter vendors in 2022, driving a significant portion of the year’s 330 GW (AC) of global inverter shipments.

Solar sovereignty: India’s path to sustainable independence and green revolution

The Indian government is actively steering the nation towards a sustainable and environmentally-conscious energy future. However, this juncture calls for a strategic alignment of protective measures to ensure their intended outcomes, notably reducing India’s reliance on energy imports and positioning the nation as a global hub for solar manufacturing.

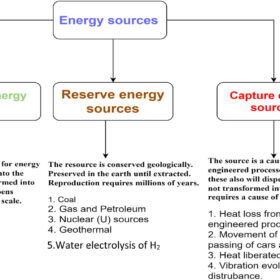

Going beyond renewable/non-renewable dichotomy

Scientists in India have proposed a new classification of energy sources that is intended for the adoption and definition of emerging technologies, which they said conventional taxonomies fail to achieve.

8.5 GW of solar parks completed under govt support scheme

Eleven solar parks aggregating 8.521 GW have been completed and seven solar parks totaling 3.985 GW partially completed under the Ministry of New and Renewable Energy’s scheme for “Development of Solar Parks and Ultra-Mega Solar Power Projects.”

Future of distributed green hydrogen in India

India can gain an edge in green hydrogen by focusing more on making its production accessible and affordable. Using the distributed business model and building an enabling regulatory framework will stimulate wider acceptance.

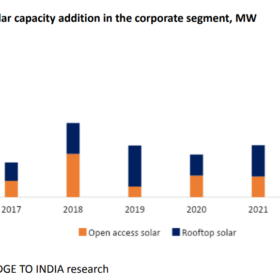

Bright prospects ahead for corporate solar market

In an exclusive article for pv magazine, Bridge To India provides a quick look at the key drivers and outlook for the corporate solar market in India.

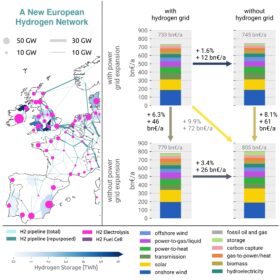

The Hydrogen Stream: Hydrogen grid could cut Europe’s energy costs by 3.4%

German researchers say gas-grid retrofits for hydrogen transport, combined with power grid expansion, could decarbonize Europe’s economy, while S&P says the global ammonia trade could expand by nearly 10 times by 2050.

India will add 45 GW of renewable energy capacity over next two fiscals, says CareEdge Ratings

India will install around 20-25 GW of new renewable energy capacity annually over the next two fiscals, driven by a healthy project pipeline and a strong bidding roadmap. The decline in solar module prices and one-year relaxation for the approved list of module manufacturers (ALMM) bode well for the capacity addition.

Solar module prices, auction volumes, and the outlook for capacity addition

Timely scale-up in tendering activity and moderation in solar PV cell and module prices, if sustained, would support improvement in capacity addition in the renewable energy sector.